India Battery Chemicals Market, By Chemical Type (Cathode Materials, Anode Materials, Electrolytes, Battery Salts & Additives ); By Battery Type (Lithium-ion Batteries, Lithium Iron Phosphate (LFP) Batteries, Lead-acid Batteries, Sodium-ion Batteries, and Others); By Production Source (Virgin Battery Chemicals, Recycled Battery Chemicals ); By End User (Automotive, Renewable Energy & Power Utilities, Electronics, Industrial Manufacturing, Telecommunications ); By Trend Analysis, Competitive Landscape & Forecast, 2019-2032

- Chemicals & Advanced Materials

- Feb 2026

- Pages 250

- Report Format: pdf

- Report Price: $2500 USD

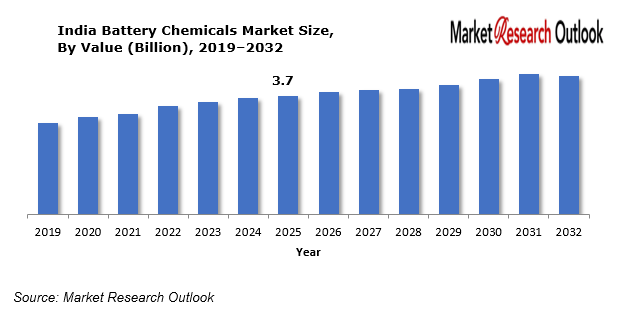

India Battery Chemicals Market Size & Forecast, 2019-2032

The India Battery Chemicals Market size was estimated at USD 3.7 Billion in 2025. During the forecast period, the India Battery Chemicals Market size is projected to grow at a CAGR of 14.2% reaching a value of USD 9.0 Billion by 2032. The market will experience increasing growth because battery supply chains are being established in local areas. The upcoming launch of multiple gigafactories together with cathode and anode and electrolyte production plants will enable the country to decrease import needs while improving its cost effectiveness. The domestic capacity of India to process essential battery materials will increase through foreign direct investment and technology partnerships and strategic alliances. The rate of electric vehicle adoption is expected to increase rapidly because it will expand from two- and three-wheelers to include passenger cars and buses and commercial vehicles. The transition will result in a major requirement for lithium-ion battery chemicals which include lithium hydroxide and carbonate and nickel and cobalt sulfates and manganese-based compounds and graphite and advanced electrolyte formulations.

Battery Chemicals – Overview

Battery chemicals serve as specialized raw materials and compounds which battery production requires to create energy storage systems and power generation equipment and to achieve electrochemical functionality. The chemicals which make up the battery essential functional elements determine all vital aspects of the battery which include capacity and efficiency and lifespan and safety and cost. Modern batteries which include lithium-ion batteries use battery chemicals that contain cathode materials which include lithium and nickel and cobalt and manganese compounds and anode materials which consist of graphite and silicon-based materials and electrolytes which contain lithium salts and solvents that permit ion transit and stability-enhancing additives and binders.

India Battery Chemicals Market

Growth Drivers

Rapid Growth of Electric Vehicles (EVs)

India is witnessing a sharp rise in electric two-wheelers and three-wheelers, followed by increasing penetration of electric passenger cars, buses, and commercial vehicles. Each EV requires a substantial volume of lithium-ion battery chemicals, including lithium hydroxide and carbonate, nickel sulfate, cobalt sulfate, manganese compounds, graphite, and advanced electrolytes. As vehicle electrification expands into higher-capacity battery segments such as buses and fleet vehicles, the intensity of chemical consumption per unit is also increasing. Moreover, rising investments in domestic battery manufacturing and gigafactories are strengthening the downstream demand for battery chemicals by reducing import dependency and improving supply chain efficiency.

Challenges

High Capital Investment Requirements

High capital investment requirements represent a major challenge to the growth of the India battery chemicals market, as establishing battery-grade chemical manufacturing facilities demands substantial upfront expenditure. Setting up plants for cathode and anode materials, electrolytes, and refined lithium salts requires advanced processing technologies, strict quality controls, and compliance with environmental and safety regulations, all of which significantly increase capital costs. In addition, the development of supporting infrastructure such as refining units, waste management systems, and reliable power and water supplies further raises investment requirements. For new entrants and smaller domestic players, securing financing and achieving economies of scale can be difficult, limiting market participation. Long gestation periods and exposure to volatile raw material prices also heighten financial risk, potentially delaying project execution.

Geopolitical Impact on India Battery Chemicals Market

The influence of the geopolitical forces on battery chemicals market in India is very realistic and practical owing to the fact that India is an importer of its own supply in the primary raw materials. Most of its lithium, nickel, cobalt, and graphite are imported by India and come mainly in the form of Australia, Chile, Argentina, China, and other regions of Africa. But in case tensions exist between nations, say in the form of trade wars, sanctions, export bans or alternation of policies in such nations, the supply of the raw materials may also be affected and will result in shortages and volatility in prices. Supply chains can also be complicated when there are changes in trade policies, an increase in tariffs or the nationalization of resources in a nation that is highly endowed with minerals. Additionally, any diplomatic tension or interference with key shipping routes also contribute to the increase in the lead time and the overall freight and insurance prices which in turn may directly affect the cost of raw materials of battery chemical suppliers in India.

India Battery Chemicals Market

Segmental Coverage

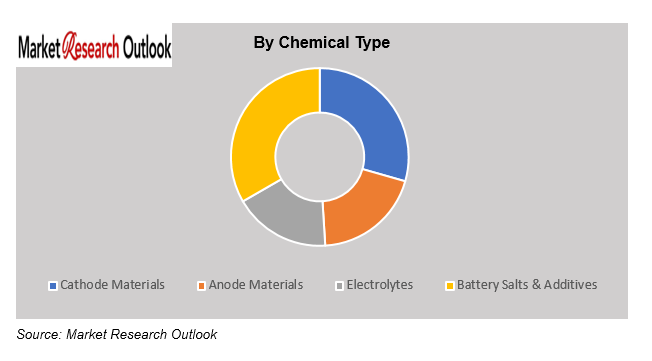

India Battery Chemicals Market – By Chemical Type

Based on chemical type, the India Battery Chemicals Market is segmented into Cathode Materials, Anode Materials, Electrolytes, and Battery Salts & Additives.

One of the most rapidly expanding sectors of the India battery chemicals market is the cathode materials segment, which is due to the rapid growth of lithium-ion battery consumables and the growing pace of electric vehicle adoption. Cathode materials contribute a major portion of the battery cost and performance and therefore, are an important area of focus given the domestic battery ecosystem of India. The growth can be driven by the increasing demand of EV batteries in two-wheelers, passenger cars, buses, and commercial vehicles, as well as, by the increasing use of stationary energy storage systems. This has increased the use of cathode-active materials, including lithium iron phosphate (LFP), nickel manganese cobalt (NMC), and nickel cobalt aluminum (NCA) which have been aided by battery materials like lithium hydroxide and carbonate, nickel sulfate, cobalt sulfate, and manganese compounds.

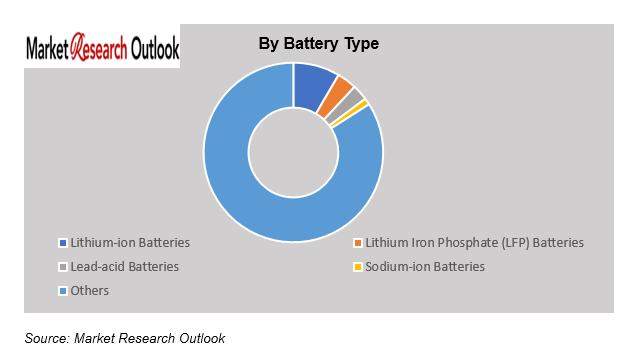

India Battery Chemicals Market – By Battery Type

Based on battery type, the India Battery Chemicals Market is segmented into Lithium-ion Batteries, Lithium Iron Phosphate (LFP) Batteries, Lead-acid Batteries, Sodium-ion Batteries, and Others. The battery chemicals market in India expands because of lithium-ion battery growth which serves as the primary driver for this market expansion since lithium-ion technology has become the dominant solution for electric mobility and energy storage and consumer electronics. The two-wheeler and three-wheeler electric vehicle market currently expands which leads to greater demand for lithium-ion battery production because people adopt electric passenger vehicles and buses and commercial fleets. The battery manufacturing process requires an increased amount of battery-grade chemicals which include lithium hydroxide and carbonate and nickel sulfate and cobalt sulfate and manganese compounds and graphite and advanced electrolytes. India now focuses on renewable energy integration which drives lithium-ion battery deployment for grid-scale energy storage and stationary energy storage systems thereby creating higher demand for these chemicals.

Competitive Landscape

Key participants in the India Battery Chemicals market include Tata Chemicals, Epsilon Advanced Materials, Himadri Speciality Chemical Ltd, Gujarat Fluorochemicals Ltd (GFL), Neogen Chemicals Ltd, Amara Raja Group, Exide Industries Ltd, Atul Ltd, Laxmi Organic Industries , BASF, and others.

These companies are implementing strategic growth initiatives in order to gain a competitive advantage. The strategies being largely adopted include mergers and acquisitions, strategic alliances, joint ventures, licensing agreements, and new product launches. With the implementation of these strategies, the market participants aim to increase product portfolios, as well as enhance regional presence for long-term sustainable business growth in the Battery Chemicals industry of India.

Scope of the Report

| Attributes | Details |

| Years Considered | Historical Data – 2019–2025

Base Year – 2025 Estimated Year – 2026 Forecast Period – 2026–2032 |

| Facts Covered | Revenue in USD Billion |

| Market Coverage | India |

| Product/ Service Segmentation | Chemical Type, Battery Type, Production Source, End User |

| Key Players | Tata Chemicals, Epsilon Advanced Materials, Himadri Speciality Chemical Ltd, Gujarat Fluorochemicals Ltd (GFL), Neogen Chemicals Ltd, Amara Raja Group, Exide Industries Ltd, Atul Ltd, Laxmi Organic Industries , BASF, and others |

Market Segmentation

- By Chemical Type

- Cathode Materials

- Anode Materials

- Electrolytes

- Battery Salts & Additives

- By Battery Type

- Lithium-ion Batteries

- Lithium Iron Phosphate (LFP) Batteries

- Lead-acid Batteries

- Sodium-ion Batteries

- Others

- By Production Source

- Virgin Battery Chemicals

- Recycled Battery Chemicals

- By End User

- Automotive

- Renewable Energy & Power Utilities

- Electronics

- Industrial Manufacturing

- Telecommunications

- By Region

- North India

- South India

- East India

- West India

- Research Framework

- Research Objective

- Product Overview

- Market Segmentation

- Executive Summary

- India Battery Chemicals Market Insights

- DROC Analysis

- Growth Drivers

- Rapid Growth of Electric Vehicles (EVs)

- Expansion of Renewable Energy & Energy Storage

- Advancements in Battery Technology

- Restraints

- Heavy Dependence on Imported Raw Materials

- High Production and Processing Costs

- Price Volatility of Key Battery Materials

- Opportunities

- Rising Demand from Consumer Electronics & Industrial Applications

- Increasing Energy Storage System (ESS) Deployments

- Challenges

- High Capital Investment Requirements

- Skilled Workforce Constraints

- Technological Advancements/Recent Developments

- Porter’s Five Forces Analysis

- Growth Drivers

- DROC Analysis

- Industry Value Chain & Entry Points

- Raw Material Sourcing

- Mineral Processing & Refining

- Precursor Material Production

- Battery Chemical Manufacturing

- Cell Manufacturing (Downstream Linkage)

- Battery Pack & Module Assembly

- End-Use Applications

- India Battery Chemicals Market: Regulatory Framework

- India Battery Chemicals Market: Marketing Strategies

- India Battery Chemicals Market Overview

- Market Size & Forecast, 2019-2032

- By Value (USD Million)

- Market Share & Forecast

- By Chemical Type

- Cathode Materials

- Anode Materials

- Electrolytes

- Battery Salts & Additives

- By Battery Type

- Lithium-ion Batteries

- Lithium Iron Phosphate (LFP) Batteries

- Lead-acid Batteries

- Sodium-ion Batteries

- Others

- By Production Source

- Virgin Battery Chemicals

- Recycled Battery Chemicals

- By End User

- Automotive

- Renewable Energy & Power Utilities

- Electronics

- Industrial Manufacturing

- Telecommunications

- By Region

- North India

- South India

- East India

- West India

- By Chemical Type

- Market Size & Forecast, 2019-2032

- North India Battery Chemicals Market Overview

- Market Size & Forecast, 2019-2032

- By Value (USD Million)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Production Source

- By End User

- Market Size & Forecast, 2019-2032

- South India Battery Chemicals Market Overview

- Market Size & Forecast, 2019-2032

- By Value (USD Million)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Production Source

- By End User

- East India Battery Chemicals Market Overview

- Market Size & Forecast, 2019-2032

- By Value (USD Million)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Production Source

- By End User

- West India Battery Chemicals Market Overview

- Market Size & Forecast, 2019-2032

- By Value (USD Million)

- Market Share & Forecast

- By Chemical Type

- By Battery Type

- By Production Source

- By End User

- Demand Outlook & Customer Adoption Dynamics

- Demand Evolution by End-Use Industry

- Purchasing Behavior & Supplier Selection Criteria

- Demand Visibility & Contracting Trends

- Regional Demand Concentration & Customer Clusters

- Competitive Landscape

- List of Key Players and Their Offerings

- India Battery Chemicals Company Market Share Analysis, 2025

- Competitive Benchmarking, By Operating Parameters

- Key Strategic Development (Mergers, Acquisitions, Partnerships, etc.)

- Geopolitical Impact on India Battery Chemicals Market

- Company Profile

- Tata Chemicals Ltd

- Introduction & Company Profile

- Product Benchmarking

- Strategic Outlook

- Key Personals

- Key Competitors

- Financial Analysis

- SWOT Analysis

- Tata Chemicals Ltd

- Market Size & Forecast, 2019-2032

- Market Size & Forecast, 2019-2032

- Market Size & Forecast, 2019-2032

**(same data pointers will be provided for the below companies)

- Epsilon Advanced Materials

- Himadri Speciality Chemical Ltd

- Gujarat Fluorochemicals Ltd (GFL)

- Neogen Chemicals Ltd

- Amara Raja Group

- Exide Industries Ltd

- Atul Ltd

- Laxmi Organic Industries

- BASF

- Other Prominent Players

- Key Strategic Recommendations

- Research Methodology

- Qualitative Research

- Primary & Secondary Research

- Quantitative Research

- Market Breakdown & Data Triangulation

- Secondary Research

- Primary Research

- Breakdown of Primary Research Respondents, By Region

- Assumption & Limitation

- Qualitative Research

* Financial information in case of non-listed companies will be provided as per availability

**The segmentation and the companies are subjected to modifications based on in-depth secondary for the final deliverable

Frequently Asked Questions

1. What is the expected growth rate of the India Battery Chemicals Market during the forecast period?

Ans: The India Battery Chemicals Market size was estimated at USD 3.7 billion in 2025.

2. What is the expected growth rate of the India Battery Chemicals Market during the forecast period?

Ans: The India Battery Chemicals Market is expected to grow at a CAGR of around 14.2% during the forecast period between 2026 and 2032.

3. What is the forecast value of the India Battery Chemicals Market by 2032?

Ans: The India Battery Chemicals Market is projected to reach a value of approximately USD 9.0 billion by 2032.

4. What are the major factors driving the growth of the India Battery Chemicals Market?

Ans: The market experiences growth because people are increasingly starting to use electric vehicles while lithium-ion battery production facilities are growing and energy storage systems are being deployed more frequently and the government provides extensive funding through PLI programs for Advanced Chemistry Cells (ACC). The market expansion receives additional support from the growing localization of the battery supply chain and the investments in gigafactories.

5. Name the key players operating in the India Battery Chemicals Market.

Ans: The key players of India Battery Chemicals Market are Tata Chemicals, Epsilon Advanced Materials, Himadri Speciality Chemical Ltd, Gujarat Fluorochemicals Ltd (GFL), Neogen Chemicals Ltd, Amara Raja Group, Exide Industries Ltd, Atul Ltd, Laxmi Organic Industries , BASF, and others.

6. Which is the fastest-growing battery type segment in the India Battery Chemicals Market?

Ans: The battery chemicals market in India expands because of lithium-ion battery growth which serves as the primary driver for this market expansion since lithium-ion technology has become the dominant solution for electric mobility and energy storage and consumer electronics.

7. Which region contributes significantly to the growth of the India Battery Chemicals Market?

Ans: Western and Southern India contribute significantly to market growth due to the presence of battery manufacturing hubs, chemical processing facilities, and strong EV ecosystem development.

Frequently Asked Questions

1. What is the expected growth rate of the India Battery Chemicals Market during the forecast period?

Ans: The India Battery Chemicals Market size was estimated at USD 3.7 billion in 2025.

2. What is the expected growth rate of the India Battery Chemicals Market during the forecast period?

Ans: The India Battery Chemicals Market is expected to grow at a CAGR of around 14.2% during the forecast period between 2026 and 2032.

3. What is the forecast value of the India Battery Chemicals Market by 2032?

Ans: The India Battery Chemicals Market is projected to reach a value of approximately USD 9.0 billion by 2032.

4. What are the major factors driving the growth of the India Battery Chemicals Market?

Ans: The market experiences growth because people are increasingly starting to use electric vehicles while lithium-ion battery production facilities are growing and energy storage systems are being deployed more frequently and the government provides extensive funding through PLI programs for Advanced Chemistry Cells (ACC). The market expansion receives additional support from the growing localization of the battery supply chain and the investments in gigafactories.

5. Name the key players operating in the India Battery Chemicals Market.

Ans: The key players of India Battery Chemicals Market are Tata Chemicals, Epsilon Advanced Materials, Himadri Speciality Chemical Ltd, Gujarat Fluorochemicals Ltd (GFL), Neogen Chemicals Ltd, Amara Raja Group, Exide Industries Ltd, Atul Ltd, Laxmi Organic Industries , BASF, and others.

6. Which is the fastest-growing battery type segment in the India Battery Chemicals Market?

Ans: The battery chemicals market in India expands because of lithium-ion battery growth which serves as the primary driver for this market expansion since lithium-ion technology has become the dominant solution for electric mobility and energy storage and consumer electronics.

7. Which region contributes significantly to the growth of the India Battery Chemicals Market?

Ans: Western and Southern India contribute significantly to market growth due to the presence of battery manufacturing hubs, chemical processing facilities, and strong EV ecosystem development.